The global economy is remarkably resilient, with most indicators pointing to a soft landing, the International Monetary Fund said in its world economic outlook on Tuesday. One caveat: Inflation, though in retreat, has yet to be tamed.

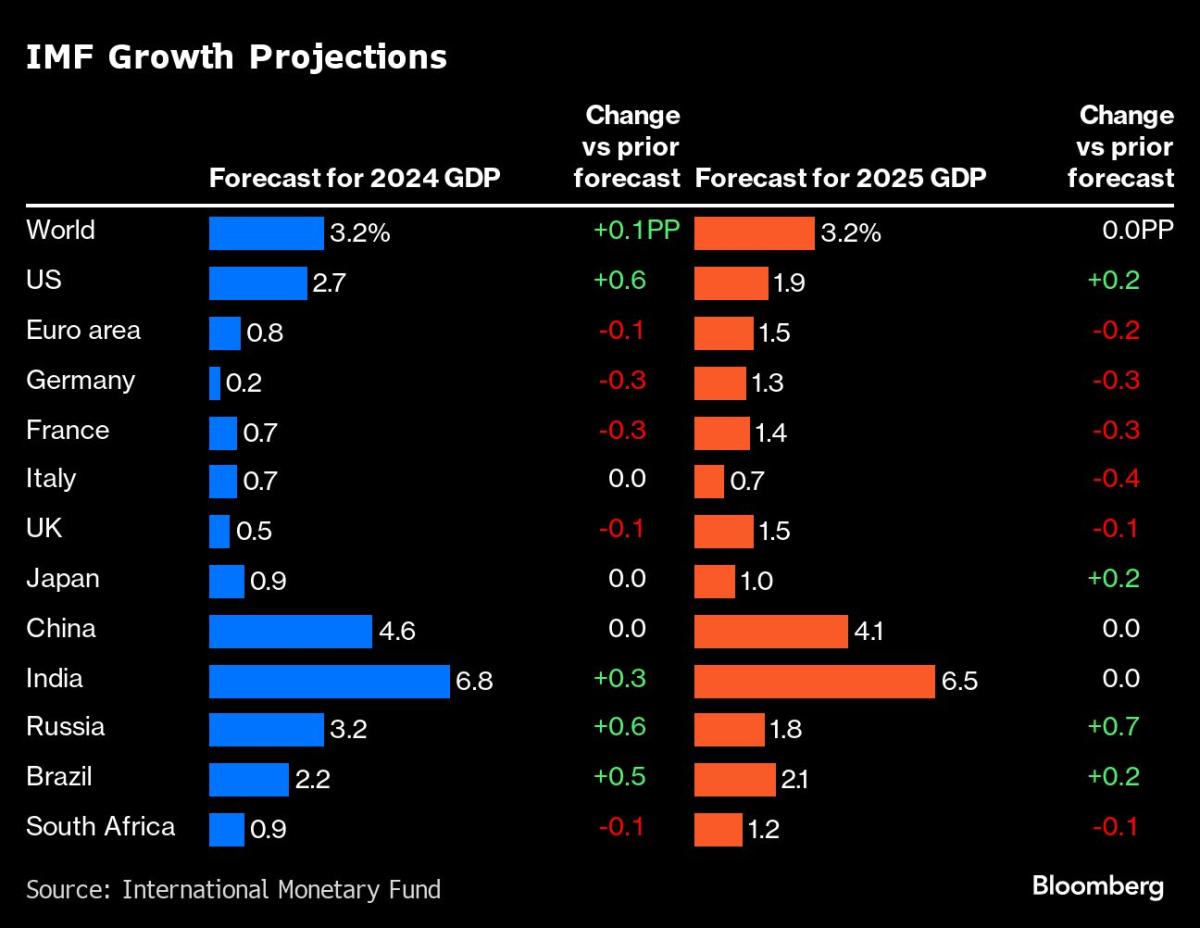

That’s a relatively upbeat outlook from the world’s chief risk watcher. Ahead of global policymakers convening this week in Washington for the spring IMF/World Bank meetings, the IMF raised its global economic growth forecast by 0.1 percentage point from its outlook in January to 3.2% this year and next.

Though resilient, global growth is anemic—and the medium-term outlook isn’t much better. The IMF expects global growth five years from now of just 3.1%. That’s the lowest medium-term growth forecast in decades. Among the drags are rising geoeconomic fragmentation, an rise in trade restrictions, and increased use of industrial policy as the U.S. and China re-evaluate their relationship and others are forced to recalibrate.

“Trade linkages are already changing as a result, with potential losses in efficiency. The net effect could well be to make the global economy less, not more, resilient. But the broader damage is to global cooperation,” IMF Chief Economist Pierre-Olivier Gourinchas says in the outlook. “There is still time to reverse course.”

The IMF expects global headline inflation to fall from an annual average of 6.8% in 2023 to 5.9% in 2024 and 4.5% in 2025. But Gourinchas urges central bankers to stay vigilant and prioritize getting back to their targets, especially as oil prices rise on the back of geopolitical tensions and services inflation continues to be sticky.

“While inflation trends are encouraging, we aren’t there yet,” Gourinchas says in the outlook. “Somewhat worryingly, progress toward inflation targets has somewhat stalled since the beginning of the year.”

Another risk: geopolitics. In a press briefing on Tuesday, Gourinchas said an escalation in geopolitical tensions that resulted in a sustained 15% increase in oil prices could boost global inflation by 0.7%. While that isn’t its base case, the IMF is keeping an eye on the situation.

China reported overnight that its economy grew at a 5.3% clip in the first quarter, faster than the IMF and others had expected. While Gourinchas said the IMF was reviewing whether it needs to raise its full-year forecast, he said indicators still showed weakness in the property sector and lackluster domestic demand.

China’s increased reliance on exports could worsen trade tensions

in an already fraught geopolitical environment, he cautioned. Indeed, Treasury Secretary Janet Yellen last week stressed concerns about China’s overcapacity and how it threatens U.S. and other foreign manufacturers as Chinese companies look to sell that oversupply abroad. Increased trade restrictions on Chinese exports could boost goods inflation, Gourinchas says.

In Europe, the IMF expects growth to rebound, but from anemic levels. While there is less risk of overheating than in the U.S., central bankers making the pivot toward monetary easing will need to pivot carefully to avoid an inflation undershoot. Though labor markets seem strong, the IMF warns that could be “illusory,” with European companies hoarding labor in hopes of a pickup in activity.

The IMF calls on policymakers to rebuild fiscal buffers. Though inflation is beginning to decline, real interest rates are still high and sovereign debt dynamics are deteriorating. So far, fiscal plans aren’t enough to build financial buffers and could be derailed further as the heavy global election calendar plays, Gourinchas says.

Also of particular concern: the U.S. fiscal stance, which the IMF says is out of line with long-term fiscal sustainability and creates both short-term risks to efforts to bring down inflation as well as longer-term fiscal and financial stability risks for the global economy. “Something will have to give,” the IMF cautioned.

{kind=link}